UX-led Zelle® for Business Ideation

With no product manager or formal brief, I identified a gap in Zelle®’s offering and initiated a UX-led concept program for small businesses. I developed 6 feature concepts, validated priorities through user interviews, and advanced the QR code experience toward launch.

01

OPPORTUNITY

Zelle® was Invisible to Business Users

Small businesses use Zelle® daily, but they use the same consumer product as P2P users. There are no designated business features, e.g. enrollment flow, business profile, invoicing. They're making workarounds inside a product that wasn't built for them.

Closing the Gaps

I initiated this effort from a UX standpoint, building on prior Zelle® workshop insights and without a product brief. I led the work end to end: identifying the gap, framing the opportunity, developing concepts, and driving user research. This is upstream, pre-roadmap work where UX helps define what should exist.

02

FEATURES

6 Features, 1 Coherent SMB Experience

Based on Zelle® SMB workshop findings and benchmarking Zelle® competitors UX, I identified 6 features to empower Zelle® business users to manage payments with trust, security and delight.

I mapped what a small business owner actually needs across the full payment lifecycle — from setting up their presence to getting paid and managing their relationships.

#1 - Zelle® Business Profile

#2 - Business Tax

#3 - Dynamic QR Code

#4 - Lite Invoice

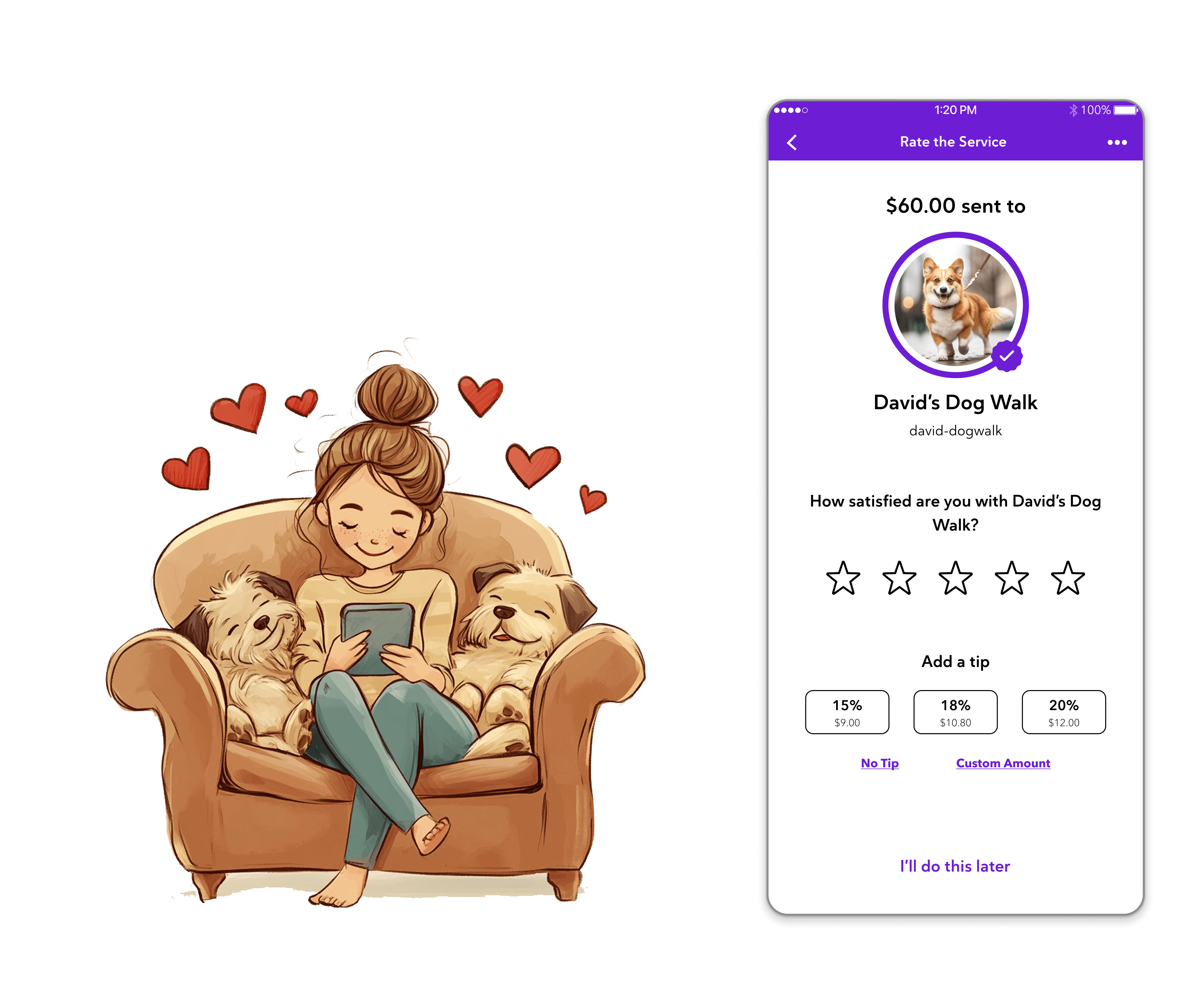

#5 - Rating & Tipping

#6 - Activity Data

03

CONCEPT VALIDATION

Evidence for Priority Decisioning

Building on the trust established by Zelle®, the business experience needed to maintain brand consistency while addressing clear user needs. After rapid prototyping, I partnered with UX research to test six feature concepts with Zelle® customers, evaluating their relevance and usefulness to inform prioritization.

16

Zelle® users interviewed across SMB concept validation

6

Feature concepts evaluated for desirability and priority

1

Feature in final design and approaching launch - QR code

Research findings show that all 6 features deliver meaningful value to business users. Zelle® QR Code, Lite Invoice, and Business Profile emerged as the highest-priority capabilities. Purchase Protection stood out as the most emotionally resonant feature, while also introducing the greatest complexity around liability and fee structures.

Zelle® QR Code advancement for business is the first priority after aligning internally with stakeholders and externally with the Advisory Board.

04

SPOTLIGHT

QR Code Design Deep Dive

The QR Code feature is the most advanced in the design process, progressing from early concept exploration through technical validation and into final UI design ahead of launch.

It directly addresses a key friction point: collecting in-person payments at the point of service. A business-branded QR code is displayed within the banking app, allowing customers to simply scan and complete payment—creating a seamless experience grounded in speed, clarity, and trust.

Advanced Dynamic QR Code Feature

Through user story mapping, I led the prioritization of a straightforward, high-impact feature first and designed a net-new Zelle® QR Code capability that allows sellers to set an amount and memo to generate dynamic QR codes. Micro-business users showed strong interest, viewing it as a lightweight invoicing tool and a mini point-of-sale solution.

Solving Friction through a Seamless Native-to-App Routing UX

Because Zelle® is embedded across 2,000+ banking apps, scanning Zelle® QR codes through native camera experiences has long created significant friction.

I led workshops with product and technical partners to define a solution that routes native camera scan results through a Zelle®-hosted URL and seamlessly directs users into their selected banking app.

The final design proposal was well received by representatives from seven owner banks, Zelle® leadership, and cross-functional stakeholders.

05

REFLECTION

What I'd Do Differently

I would initiate earlier alignment with two Zelle® owner banks to establish partnerships for A/B testing. Currently, native camera QR code scan data is incomplete, which makes it difficult to accurately measure before-and-after impact of the UX improvements. I also discovered that seven owner banks do not track click-through data for the QR code feature within their banking apps.

With earlier awareness, I would have ensured baseline data tracking was defined from day one of the design kickoff, enabling clearer measurement of performance changes from pre-launch through post-launch.

BACK TO